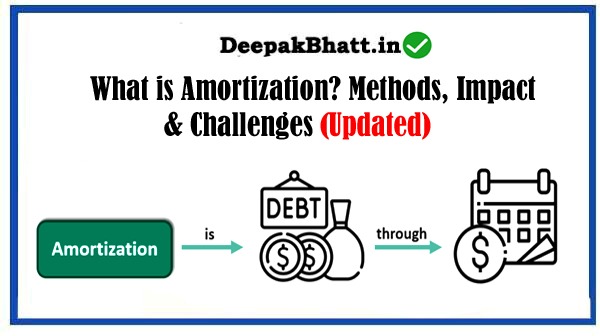

What is Amortization: An accounting technique used to systematically allocate the cost of an intangible asset or a liability over a specific period.

Unlike depreciation, which applies to tangible assets, amortization deals with non-physical assets or liabilities with a finite useful life.

The process involves distributing the cost over multiple periods, reflecting the consumption or reduction in value of the asset or liability over time.

- 1 What is Amortization in Practice

- 1.1 1. Intangible Assets:

- 1.2 2. Loan Repayments:

- 1.3 3. Mortgages:

- 1.4 4. Deferred Charges:

- 1.5 Methods of Amortization

- 1.6 1. Straight-Line Amortization:

- 1.7 2. Declining Balance Amortization:

- 1.8 3. Sum-of-the-Years-Digits Amortization:

- 1.9 4. Units of Production Amortization:

- 1.10 Impact on Financial Statements

- 1.11 1. Income Statement:

- 1.12 2. Balance Sheet:

- 1.13 3. Cash Flow Statement:

- 1.14 Real-World Applications and Examples

- 1.15 1. Intangible Assets:

- 1.16 2. Loan Repayments:

- 1.17 3. Mortgages:

- 1.18 4. Deferred Charges:

- 1.19 Challenges and Considerations

- 1.20 1. Estimating Useful Life:

- 1.21 2. Residual Value:

- 1.22 3. Regulatory Changes:

- 1.23 4. Intangible Asset Impairment:

- 1.24 Future Trends in Amortization

- 1.25 1. Technology-Driven Accuracy:

- 1.26 2. Sustainability Considerations:

- 1.27 3. Global Harmonization:

- 1.28 Conclusion

What is Amortization in Practice

Amortization finds application in various financial contexts, including:

1. Intangible Assets:

Businesses often acquire intangible assets such as patents, copyrights, trademarks, and goodwill. Amortization allows them to recognize the expense of these assets over their estimated useful lives.

2. Loan Repayments:

When individuals or businesses borrow money and repay it in installments, each installment includes both principal and interest. The portion allocated to reducing the outstanding loan balance is an amortization of the loan.

3. Mortgages:

In the context of mortgages, amortization refers to the gradual repayment of a home loan through regular monthly payments. These payments consist of both principal and interest, with the principal amount increasing over time.

4. Deferred Charges:

Certain expenses, such as organizational costs or prepaid expenses, may be capitalized and amortized over the period of expected benefit.

Basics of Personal Finance: Getting Started on the Right

A Personal Finance Guide Tutorials for Free

Learn Personal Finance 101 Free Video Course

Methods of Amortization

The method used to amortize an asset or liability depends on its nature. Common methods include:

1. Straight-Line Amortization:

The straight-line method evenly spreads the amortization expense over the asset or liability’s useful life. It is simple and easy to calculate, making it a popular choice for many scenarios.

2. Declining Balance Amortization:

Similar to declining balance depreciation, this method frontloads the amortization expense, with higher amounts recognized in the earlier periods. As the asset’s value diminishes, the amortization expense decreases over time.

3. Sum-of-the-Years-Digits Amortization:

This method accelerates the amortization process, with a higher expense in the earlier years. It is calculated using a formula that considers the sum of the years’ digits of the asset or liability’s useful life.

4. Units of Production Amortization:

This method ties the amortization expense to the actual usage or production of the asset. The more the asset is used or produces, the higher the amortization expense.

Impact on Financial Statements

Amortization has a notable impact on a company’s financial statements, influencing both the income statement and the balance sheet:

1. Income Statement:

On the income statement, amortization is recognized as an expense. This reduces the reported profit, aligning with the matching principle by spreading the cost over the periods in which the asset contributes to revenue.

2. Balance Sheet:

On the balance sheet, the amortized asset is reported at its net book value, which is the original cost minus the accumulated amortization. This provides a more accurate representation of the asset’s economic value.

3. Cash Flow Statement:

While amortization is a non-cash expense, it is not added back to the operating cash flow section of the cash flow statement. Unlike depreciation, which is added back, amortization is treated as a permanent reduction in the value of the asset.

Real-World Applications and Examples

1. Intangible Assets:

Consider a software development company that acquires a license for a proprietary software. The cost of the license is amortized over the software’s expected useful life.

2. Loan Repayments:

Individuals with car loans or business loans make regular monthly payments. A portion of each payment goes towards reducing the outstanding loan balance, representing amortization.

3. Mortgages:

Homeowners making mortgage payments are engaged in the amortization process. Initially, a larger portion of the payment goes towards interest, but over time, more is applied to reduce the principal.

4. Deferred Charges:

A company may incur costs associated with setting up a new facility or entering a new market. These organizational costs can be deferred and amortized over the period of expected benefit.

Challenges and Considerations

While amortization is a widely used and accepted accounting practice, businesses need to navigate certain challenges and considerations:

1. Estimating Useful Life:

Determining the useful life of an intangible asset involves judgment and estimation. Changes in technology or market conditions can impact the accuracy of these estimates.

2. Residual Value:

Similar to depreciation, the concept of residual value in amortization is crucial. Accurate estimation is necessary for calculating amortization, and unexpected changes in value can impact financial reporting.

3. Regulatory Changes:

Accounting standards related to amortization may change over time. Businesses need to stay informed about regulatory updates to ensure compliance.

4. Intangible Asset Impairment:

If the value of an intangible asset declines significantly and is not recoverable, businesses may need to recognize an impairment loss, impacting the asset’s carrying amount and potentially necessitating adjustments to the amortization schedule.

Future Trends in Amortization

1. Technology-Driven Accuracy:

Advancements in technology, including artificial intelligence and machine learning, may enhance the accuracy of estimating useful lives and predicting changes in the value of intangible assets.

2. Sustainability Considerations:

As sustainability gains prominence, businesses may consider incorporating environmental, social, and governance (ESG) factors into the amortization of intangible assets.

3. Global Harmonization:

Efforts toward global accounting standards may lead to greater standardization in amortization practices across different regions, improving comparability for investors.

Conclusion

In conclusion, amortization is a cornerstone of financial accounting, facilitating the systematic allocation of costs over time.

Whether applied to intangible assets, loan repayments, or deferred charges, amortization plays a vital role in financial reporting and decision-making.

As businesses navigate the complexities of financial management, a clear understanding of amortization is essential for accurate and transparent financial statements.